Deadline for deregistration of cash registers with the tax authorities. The procedure for deregistering cash registers with the tax authorities. How to deregister an online cash register with the tax authorities yourself, voluntary closure

Removal of cash registers from tax registration

In order to remove a cash register from registration with the Federal Tax Service, the following conditions are necessary:

All data must be transferred to the OFD.

The FN archive must be closed at the checkout.

To do this, it is necessary that the tariff is valid at the checkout (activation code or annual\quarterly\three-yearly). A cash register connected to the Internet will transfer previously unsent documents. After which you can proceed to the procedure for closing the FN archive at the checkout. This is done through the cash register driver installed on the computer to which the cash register is connected, or by a sequence of commands described in the manual specific model KKT. After the FN archive is closed, you need to make sure that it is transferred to the OFD and there is no data left to be transferred to the OFD at the checkout. If everything is so and the report on closing the fiscal fund is displayed in the list of receipts in the “cash register monitoring” section and the cash register itself is in the status “fiscal fund archive is closed,” you can turn off the cash register and remove the fiscal drive from it.

If the cash register is activated by a quarterly, annual or three-year tariff in the OFD, it is necessary to stop the tariffication of the cash register in the “cash management” section. The remaining funds will be returned to your balance personal account. It can be used to activate another cash register or make a refund through the accounting department. If the cash register is activated with an activation code, it is impossible to stop the tariff, transfer it or return the money for it, it is also impossible.

The fiscal drive is subject to responsible storage within 5 years from the date of closing the archive and may be required by the tax office. After deregistration of the cash register with the tax office, the cash register itself can be re-registered with a new FN to another organization (the cash register can be sold).

To remove a cash register from registration with the NFS, you must go to the taxpayer’s personal account on the website nalog.ru and remove the cash register from tax registration; this will require data from the closure report (date, time, fiscal indicator).

It should be noted that in the OFD Personal Account, the status “deregistered” is not displayed, the Federal Tax Service does not return information to the OFD about this status. Thus, the state “FN archive is closed” is final.

For ease of navigation through your Personal Account, in the “Cash register monitoring” section, you can create an additional point of sale (button + point of sale) and transfer deregistered cash registers to it. The name of such a retail outlet is used arbitrarily (example: “discounted”, “written off”...). Using the hierarchy of access rights to retail outlets for users, you can deny users access to such a retail outlet and the cash registers containing it. This way, personal account users will see only active cash registers. Important: - the administrator (creator of the Personal Account) sees everything retail outlets and all system modules personal account.

Deregistration of a cash register is necessary if the cash register is no longer needed, is transferred to another legal entity or individual entrepreneur, is stolen or lost.

There are three ways to apply for deregistration: in person at tax office, on the Federal Tax Service portal or in the personal account (PA) of the fiscal data operator. Users of Kontur.OFD can deregister the cash register from the tax office independently in their personal account.

Before deregistering the cash register, generate a report on closing the fiscal accumulator (FN) at the cash register. If the Federal Tax Service is broken and the report has not been generated, the cash register can only be deregistered through the Federal Tax Service. You can close the FN using a utility for registering a cash register on your computer.

If the cash register is stolen or lost, file a statement with the police and receive a certificate of registration of the statement. This certificate is needed when re-registering a cash register through a branch of the Federal Tax Service.

If you apply online, no supporting documents are needed.

Deregistration of an online cash register through the Federal Tax Service

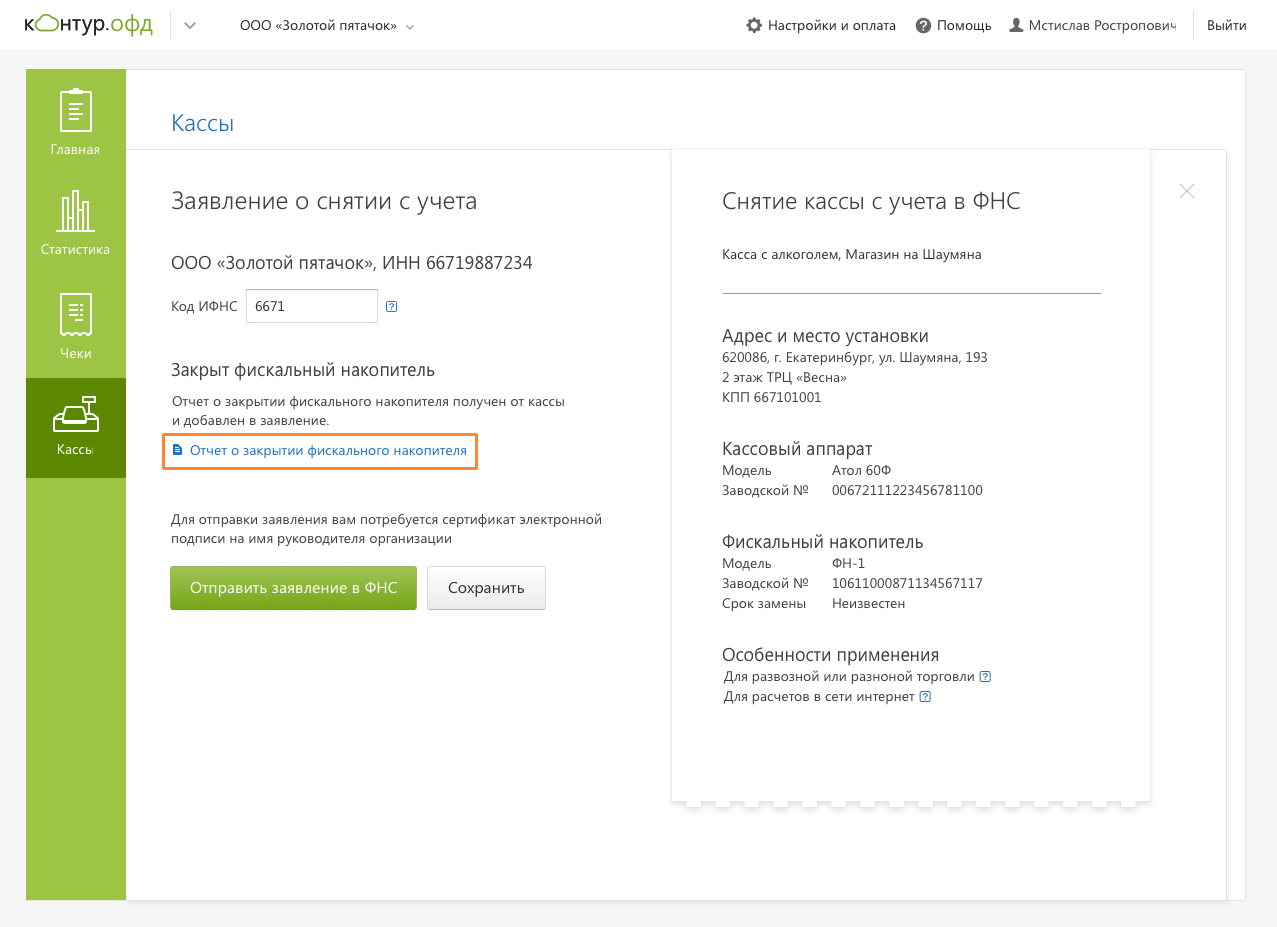

- In the “Cashiers” section in the Kontur.OFD account, go to the cash register card and click the “Deregister with the Federal Tax Service” button.

- Enter the Federal Tax Service code. Data from the report on the closure of the fiscal drive will appear in the application automatically if the cash desk has a connection to the OFD and Internet access.

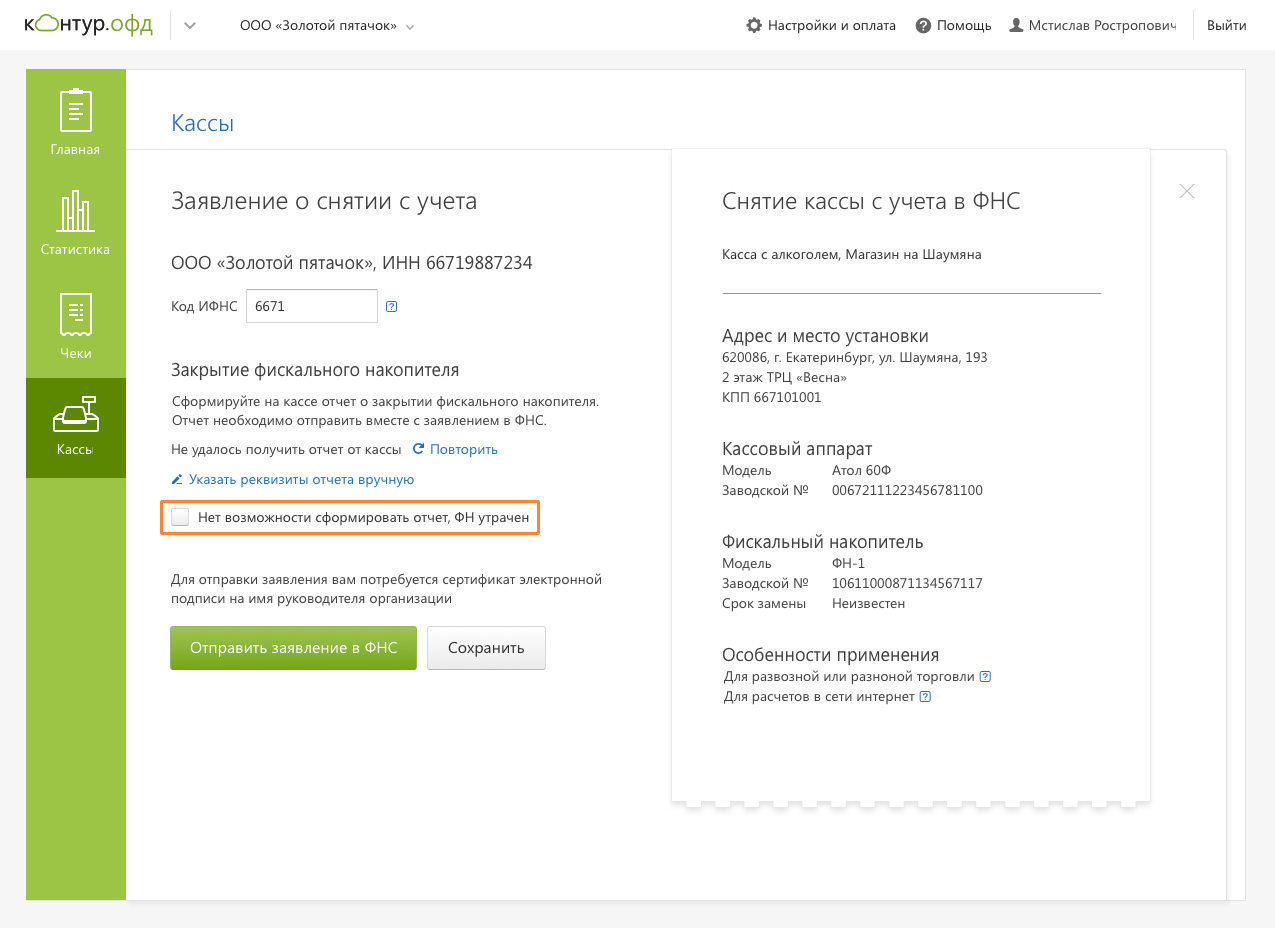

- If the cash register does not have a connection with the OFD and the report on closing the financial fund does not appear in the application, you can specify its parameters manually.

The date, time and other parameters must be taken from the printed report on closing the financial fund.

- If it is not possible to generate a report on the closure of the financial fund due to the loss or theft of the cash register, please indicate this.

- Sign the application electronic signature the head of the company and send it.

The authority has 10 working days to respond from the submission of the application to Kontur.OFD.

When the Federal Tax Service approves the application, a withdrawal card will be sent to the LC. The card has been generated - the cash register has been deregistered.

Many individual entrepreneurs use a cash register (KKM) in their activities. But a situation may arise when a cash register needs to be deregistered. In our publication today, we will tell our readers how to deregister cash registers with the tax service.

The need to deregister a cash register with the tax office may arise in the following cases:

- When replacing an old cash register with new device.

- Due to expiration date operation of cash registers(the cash register came out of the state register).

- When closing an individual entrepreneur ( legal entity), and the cash register is listed in the State Register.

- When selling cash register there was a change in the owner of KKM.

In addition to the above reasons for deregistering a cash register, starting from July 2017, all old-style cash registers must be deregistered in order to be replaced with online cash registers. This is defined in the provisions of the law of May 22, 2003 No. 54-FZ.

Based on the provisions of Law No. 54-FZ, if as of July 1, 2017, an enterprise or individual entrepreneur has a registered old-style cash register, and the enterprise or individual entrepreneur has not taken measures to purchase and install new technology, the tax authorities will not deregister it unilaterally. But in addition to this, the Federal Tax Service, according to the Federal Tax Service letter No. ED-4-20/11625@ dated June 19, 2017, has the right to impose a fine on the owner of an old-style cash register.

Documents for deregistration of old-style cash register machines

Please note that it is mandatory to deregister the cash register with the tax office!

In order to deregister a cash register with the tax office, it is necessary to prepare the appropriate package of documents, namely:

- application for deregistration of a cash register (form);

- KKM passport;

- registration card for the cash register;

- journal of the cashier-operator (form No. KM-4);

- book of income and expenses (for individual entrepreneurs);

- cash book (for legal entities);

- act from the central service center (form No. KM-2);

- block content reports fiscal memory(the last check punched on the cash register machine).

Please note that the list of the above documents may change. Exact list It is better to check the documents for deregistration of cash registers with the tax office at the place of registration of the individual entrepreneur.

The procedure for deregistering cash register machines with the tax office

After you have collected the necessary package of documents, you can go to the tax office. When deregistering a cash register, the tax inspector must check the information in the cashier-operator’s journal with the data specified in the fiscal memory report. This action is performed by a mechanic in the presence of an inspector.

After reconciling the data, the tax inspector gives permission to the mechanic to close the ECLZ memory unit. From now on, it is impossible to punch a receipt at the checkout. The EKLZ block must remain with the individual entrepreneur for 5 years.

By the way, you can ask the mechanic to remove the cash register without your personal presence.

From the moment the inspector makes a corresponding note in the tax database, the cash register is considered closed.

After completing the procedure for deregistering the cash register with the tax office, you can deal with the cash register at your discretion: sell it, keep it, or give it to someone else.

After carrying out this procedure, it becomes impossible to work on the cash register, and after submitting this report with a set of documents to your tax office, the inspector puts a corresponding mark in the tax database and the cash register is considered closed.

The procedure for deregistering an online cash register with the tax authorities

Reasons for voluntary deregistration of an online cash register:

- transfer of a cash register to another owner;

- loss or theft of cash register;

- KKM malfunction beyond repair.

Reasons for forced deregistration of online cash register machines unilaterally by the Federal Tax Service:

- expiration of the fiscal attribute key at the Federal Tax Service;

- non-compliance of cash register with the requirements of current legislation.

In the first case of deregistration of the cash register, the user is obliged to provide to the Federal Tax Service Inspectorate all fiscal data stored in the cash register within a month from the date of deregistration of the cash register.

In the second case of forced deregistration of the cash register, the cash register can be re-registered after eliminating the identified deficiencies.

Deadline for submitting an application for deregistration of an online cash register (or cash register)

If you voluntarily deregister a cash register with a fiscal register (transfer to another owner, breakage, theft or loss of an online cash register), you must deregister the cash register with the INFS within one business day.

Documents for deregistration of online cash registers

There are two ways to submit an application for deregistration of a cash register online:

- on the Federal Tax Service website through the taxpayer’s personal account;

- personally visiting the Federal Tax Service.

It is worth noting that deregistration of a new generation cash register with a fiscal registrar is much simpler than deregistration of an old-style cash register.

Attention! This material is about how to withdraw cash registered with the tax authorities. If you are interested in how to withdraw a Z report from the cash register (regular cash withdrawal), click!

Entrepreneurial activity is not always simple and cloudless. Sometimes it happens that you have to wind down your business, but that’s all work equipment store in the far corner. But if counters, furniture, computers, etc. can simply be hidden away or tried to be resold, then with cash register equipment we need to do things differently.

Before you finally put it on the shelf or put it up for sale, it must be deregistered with the tax office.

Moreover, this should be done not only in case of business closure, but also in some other situations. Let's look at this topic in more detail.

We remove cash register equipment from registration: reasons

The need to completely deregister cash registers with the tax authorities or re-register them may arise under a variety of circumstances. It could be:

- liquidation of a legal entity (enterprise or organization) as well as closure of an individual entrepreneur;

- voluntary replacement of a cash register with a more functional and new model;

- forced replacement of outdated cash register equipment due to the fact that she was deleted from the list state register. The cash register can be used for no more than 7 years from the date of its release.;

- theft of cash register equipment. In this case, you will need to present a police certificate to the tax specialist;

- leasing, donating, or selling to another company or individual entrepreneur;

- force majeure (fires, floods, destruction of buildings, etc.);

- changes in the relevant part of the legislation;

- in cases where the cash register is not used for any reason. This is especially important if its further use is also not planned, but at the same time, both company employees and outsiders have access to it. To avoid unauthorized and uncontrolled use of the cash register, it must be deactivated.

Why deregister cash registers with the tax authorities?

It is necessary to deregister cash registers with the tax authorities, regardless of what caused the cessation of their use. It is necessary to remember that data about each fiscal registrar or cash register used is in the database tax service. And if so, it means they must undergo regular maintenance and timely maintenance.

If the cash register has not been deregistered, representatives of the tax office can stop by at any time to check for correct issuance cash receipts buyers or consumers of services.

This is especially true for individual entrepreneurs, since they are the easiest to find if something happens (at the place of residence indicated when registering the individual entrepreneur with the Federal Tax Service). The most unpleasant thing will be if a representative of the organization or individual entrepreneur will not be able to answer the question of where the cash register equipment registered to his company is located.

And of course, it is worth remembering that without deregistering the cash register with the tax service, it cannot be sold or donated.

The procedure for removing cash register equipment from registration

In short, the process of removing cash registers from tax accounting occurs in several stages:

- preparation of a set of documents;

- consulting and involving a service center employee in the procedure;

- visit to the tax office.

If everything is done in order and correctly, then the process of deregistering the cash register will take no more than half an hour.

What is important when deregistering a cash register?

The main point of the operation to deregister a cash register with the tax authorities is so that they can check how consistent the information in the cash register is with the information in the fiscal memory, as well as the subsequent deactivation of the device and the transfer of ECLZ data for storage. It should be noted here that there is no strict regulation of this procedure, therefore each region of the Russian Federation regulates this process in its own way.

Before going to the territorial department of the tax service, you need to clarify what specific requirements are imposed on the procedure for deregistering a cash register from the very department of the Federal Tax Service in which it was registered.

Attention! Sometimes tax authorities require that the removal of fiscal reports from cash register equipment be carried out only in the presence of their representative. In this case, you need to negotiate in advance with an engineer from the center maintenance that he could drive up to the tax office at a certain time. An individual entrepreneur or an employee of a company submitting an application to deregister a cash register must have everything with them necessary documents and the cash register itself.

It should be noted that not all territorial inspectorates are so strict about this process. Some do not require cash registers to be brought to them and invitations technical specialist, they are limited to checking documents, the main thing of which is the correct execution and resolution of a certified technical center.

In even more simplified schemes, service center employees independently remove the EKZL block and collect all the documents for deregistering the cash register with the tax office. In this case, the owner of the cash register only needs to go to the tax office in person with an application or send a representative there with a power of attorney. This must be done either on the same day, or, if this is established in the rules of the local territorial tax office, within three days.

Before removing a cash register from tax registration, you must make sure that all tax reporting Currently, it has been submitted on time, there are no debts to the tax authorities, all bills from the organization servicing the equipment have been paid.

In addition, it would not be amiss to once again check the correctness of entering information into the cashier-operator’s log and check the technical maintenance log.

Documents for withdrawing cash registers for the tax authorities

After all the necessary preliminary checks and the operations have been completed, it’s time to start creating a package of documents for the tax office. It includes several important documents, without which deregistration of the cash register is impossible. Here is a list of these documents:

- card issued upon registration of a cash register with the tax office;

- personal passport of the applicant or representative by power of attorney;

- technical passport of cash register equipment and separately a passport of the EKLZ unit;

- cashier-operator's journal;

- technical specialist call log;

- a copy of the balance sheet certified by the tax inspectorate for the last reporting period;

- from LLC;

- book of income and expenses from individual entrepreneurs.

The last two documents are not required, but in some cases the tax inspector may ask for them for a full analysis of the cash register information.

From a service center employee, tax authorities will require:

- a receipt with a fiscal report for the entire period of use of the cash register;

- act on taking cash counter readings;

- one check report for each of the last three years of operation of the cash register;

- monthly fiscal reports also for a three-year period;

- receipt confirming the closure of the device’s memory archive;

- report on the EKLZ memory block;

- act on the transfer of EKLZ for storage. By the way, it must be stored for at least five years from the moment the cash register is deregistered in case of a possible tax audit.

After all of the above documents have been given to the tax inspector, and the procedure for deregistering the cash register has been completed, you can do whatever you want with the cash register: sell, rent, give to the commission department of the technical center, donate, simply put in corner. However, it is worth remembering that if a cash register model is deleted from the state register, its further use will be impossible. In this case, you can only throw away the cash register.

In this article we will look at how to deregister cash registers in 2020. Let's figure out whether it is necessary to deregister the KKM. Let's find out when to deregister. We will analyze the necessary documents for withdrawal.

Is it necessary to deregister a cash register and in what cases? This issue puzzles many entrepreneurs and organizations using cash register systems. Today we will talk about the procedure for deregistering a cash register: in what cases a cash register should be deregistered, what documents are required for this, how to check the registration of a cash register with the Federal Tax Service. We will also consider in detail typical situations of deregistration of cash registers and provide answers to common questions.

Who is required to use KKM

According to Federal Law No. 54, individual entrepreneurs and legal entities that carry out settlements with buyers and sellers both in cash and non-cash have obligations to use cash registers (CCM). In particular, business entities are required to have a cash register when:

- sales of goods (works, services) to organizations and the population;

- payment of funds in favor of the population and/or legal entities when purchasing goods/services;

- refund to the buyer if the goods are rejected;

- receiving money from the seller for the returned goods.

When do you need to deregister a cash register?

In addition to the obligations to use CCP, federal law No. 54 also regulates the mechanism for registering and deregistering cash registers. According to the law, you should contact the Federal Tax Service to deregister the cash register in the following cases:

- The cash register has been sold. If you sold your own cash register, it should be deregistered, after which the purchasing company is obliged to register the equipment in its name;

- The depreciation period of the cash register has expired. For each model of cash register equipment, it is installed own term beneficial use. In the month following the depreciation expiration period (100% depreciation), the unit of equipment must be deregistered;

- The individual entrepreneur (legal entity) has ceased its activities. In this case, we are not talking about a temporary break in activity, but about its complete cessation (liquidation, reorganization, closure of individual entrepreneurs, etc.). If you have documents on the closure of an individual entrepreneur (liquidation of a legal entity), then you need to contact the Federal Tax Service to deregister the equipment that was registered with the business entity;

- The cash register has been replaced with a different model. If, for one reason or another, you decide to change the cash register to another piece of equipment (for example, to a newer model), then old device You should be deregistered in the prescribed manner. Also, the deregistration procedure is provided for cases of replacing faulty equipment with working equipment (the faulty cash register is deregistered, the new device is registered with the organization);

- The cash register has been stolen. The mandatory procedure in case of cash register theft is deregistration of the cash register. The basis for removal is a certificate issued by the Ministry of Internal Affairs stating that the CCP is wanted;

- Other reasons why further use of CCP is impossible. In the process of conducting business, a business entity may encounter other situations in connection with which the use of cash registers is not possible. Subject to availability objective reasons and supporting documents, the organization/individual entrepreneur should contact the Federal Tax Service to deregister the cash register.

We remove cash registers from registration: instructions and documents

The deregistration of a cash register, as well as the registration of a cash register, is carried out through the Federal Tax Service. Before contacting the tax office, you should prepare the following documents:

| No. | Document | Description |

| 1 | Statement | The main document for deregistration of a cash register is an application. The document is drawn up on the form KND-1110021, which is also used when registering a cash register. The form should contain the following basic information: · applicant’s details (company name/full name of individual entrepreneur, TIN code, foreign trade code, place of registration, contact details); · code of the tax authority to which applications are submitted; · note on deregistration of cash registers (code “2”); · data on the cash register (model, serial number, registration data, information about the place of registration); · information about the organization performing maintenance of the cash register (name, tax identification number, date and number of the contract, data on the visual control device). The document can be filled out by hand or drawn up in electronic form(on the Federal Tax Service website in your personal account). |

| 2 | Registration certificate | When submitting documents to deregister a cash register, you must have a valid technical passport for the equipment that you plan to deregister. |

| 3 | Registration card | The original and a copy of the card issued to the entrepreneur/legal entity when registering the cash register is submitted to the Federal Tax Service. The document must be drawn up in the form approved by order of the Federal Tax Service of the Russian Federation No. MM-3-2/152 dated 04/09/2008. |

| 4 | Cashier's journal | The list of documents required to deregister a cash register includes the Operator's Journal, which is filled out on a daily basis. |

| 5 | Account coupon | Before submitting documents, contact the service center where the cash register is serviced and request a copy of the registration coupon for the cash register for subsequent presentation to the Federal Tax Service. |

| 6 | Applicant's passport | When submitting documents, the applicant must have a passport with him: for individual entrepreneurs - the entrepreneur’s passport, for legal entities - the passport of the authorized person who deregisters the equipment. |

Having collected the necessary documents, proceed directly to the procedure for deregistering a cash register:

Step 2. Transfer of documents to the Federal Tax Service.

To deregister a cash register, you need to contact the Federal Tax Service with which the cash register is registered. You can submit documents in any of the following ways:

- Go to the tax office in person and hand over the documents to a Federal Tax Service specialist. This method reliable, because you will be sure that the documents are transferred to their destination. In addition, a tax specialist will be able to conduct an initial check of documents and immediately point out to you the presence of errors and inaccuracies;

- Send the documents by mail. You can send the collected package of documents by letter through the nearest Russian Post office. Before sending, make a list of attachments, and then issue a notification letter. Having received the documents, the Federal Tax Service specialist will put a signature on the spine of the letter, which will serve as confirmation of their receipt;

- Submit an electronic application. If you have access to the Internet, you can deregister your cash register without leaving your home. To do this, register on the State Services Internet resource (gosuslugi.ru) and fill out an electronic application through your Personal Account.

Step 3. Review of documents.

The Federal Tax Service has 5 working days to consider the application and deregister the cash register. During this time, a fiscal service employee must contact you to agree on the time and place for taking control readings from the equipment. On the appointed day, in the presence of you and the Federal Tax Service specialist, the central control center engineer takes the CCT readings. Also, in your presence, an act is drawn up.

Step 4. Deregistration of cash registers.

Based on the documents you provided, as well as the KM-2 act, drawn up in your presence, the Federal Tax Service enters into the database information about the deregistration of the cash register. You are provided with a passport for the cash register and a cash register registration card with marks from the Federal Tax Service on deregistration of the equipment.

Typical situations

The most common situations for deregistration of a cash register is the cessation of business activities associated with the liquidation of an LLC or the closure of an individual entrepreneur. In each of the above cases, deregistration is carried out in general procedure. In this case, an extract from Rosreestr on the termination of the activities of an individual entrepreneur or legal entity should be additionally attached to the package of documents.

Another reason for deregistration of a cash register may be the loss of documents for a cash register. In general, when deregistering a cash register, a business entity should restore lost documents. If we are talking about a technical passport and a cash register registration card, then the individual entrepreneur/legal entity should contact the service center to obtain duplicate documents. If you lose your registration card, this information should be indicated in the application. Since the second copy of the card is located at the Federal Tax Service, where the application is submitted, there is no need to request a duplicate card. If an organization has lost the Cashier's Journal, then it is necessary to deregister the cash register based on accounting data and daily Z-reports.

How to check registration of cash register with the Federal Tax Service

How to deregister a cash register: questions and answers

Question No. 1. Individual Entrepreneur Kukushkin submitted documents to the Federal Tax Service to deregister the cash register. The tax specialist demanded that Kukushkin show the cash register (bring it to the tax office). Are the actions of the Federal Tax Service legal?

Answer: The requirements of the Federal Tax Service specialist in this case do not contradict current legislation. As a rule, tax authorities inspect the cash register when control readings are taken by a control center engineer. However, in exceptional cases, a fiscal service employee may require the presentation of the cash register directly to the inspectorate.

Question No. 2. Individual Entrepreneur Soloviev personally handed over to the Federal Tax Service a set of documents for deregistration of the cash register. What is confirmation for Solovyov that documents have been accepted?

Answer: Having received documents from Solovyov, the fiscal service employee can issue a receipt for receipt of the papers. If Soloviev draws up an application in 2 copies, then he can keep one of them (with a receipt mark, date and signature of the responsible employee of the Federal Tax Service) as confirmation.

Question No. 3. Kashtan LLC has an old cash register that is not used in its business. What documents must be submitted to Kashtan to deregister the cash register?

Answer: Removal of old cash desks from registration is carried out in accordance with the general procedure. The fact of non-use of the cash register in activities is confirmed by the operator’s log and the Z-report taken by the central service station employees.